Why Is the US Tax Code So Complicated? (It's Not an Accident)

- Mar 10

- 6 min read

Updated: Mar 18

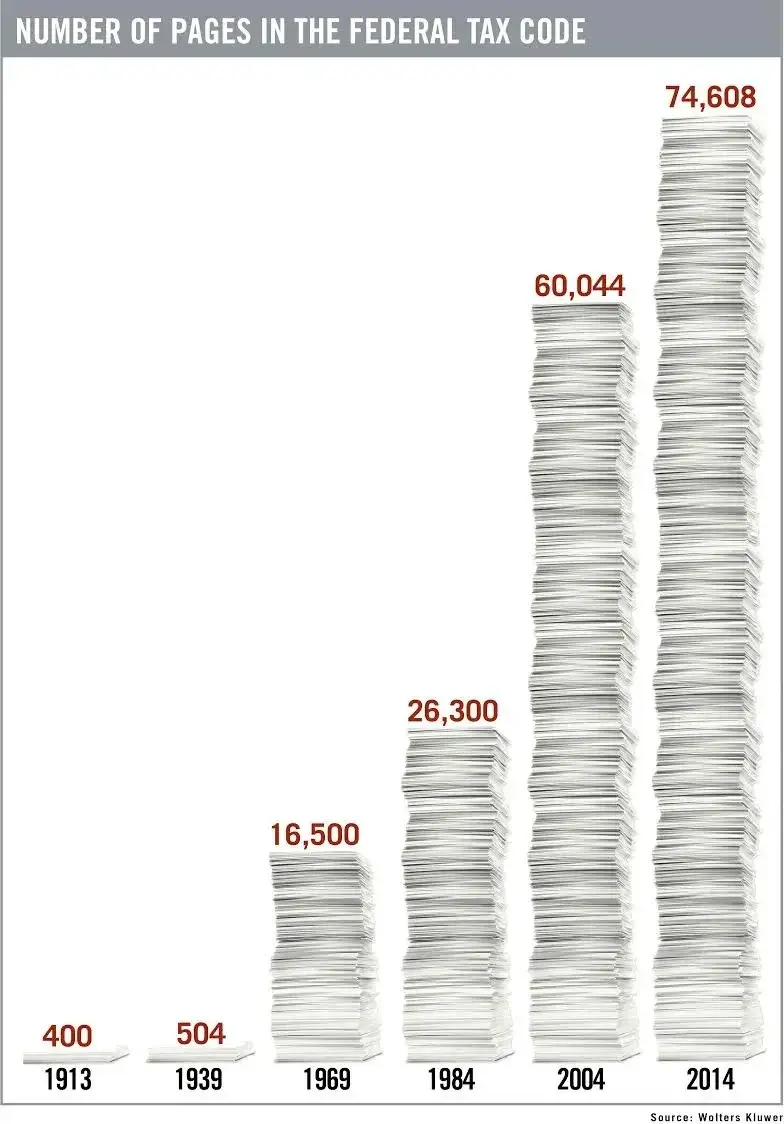

The United States tax code is approximately 70,000 pages long. Professional accountants with decades of experience get it wrong. The IRS has run studies where they give the same tax return to multiple professional preparers and get different answers every time.

There are literal competitions where certified tax professionals file the same hypothetical return and virtually no one arrives at the same number.

None of this is an accident. The complexity is a feature - not a bug.

First: The Basic Injustice Nobody Explains Clearly

If you earn money by working, getting a paycheck, freelancing, running a business, you pay ordinary income tax rates.

In 2025 those rates top out at 37% for income above $609,000 for single filers.

If you earn money by owning things like stocks, real estate, other assets held for more than a year, you pay long-term capital gains rates. Those top out at 20%. For most middle-class investors, the rate is 15%.

So a teacher earning $80,000 a year pays a marginal rate of 22% on their income. A hedge fund manager earning $80 million from carried interest 20%. The person doing the work pays more, proportionally, than the person whose money does the work.

Warren Buffett has pointed this out for decades. He famously noted that his secretary paid a higher effective tax rate than he did. This wasn't whining — it was a structural observation about how the system is designed.

Why Does Capital Get Preferential Treatment?

The official justification for lower capital gains rates has three components:

Investment risk: Capital gains represent returns on risk-taking. Taxing them too heavily discourages investment, which discourages economic growth.

Inflation adjustment: If you buy a stock for $10 and sell it for $15 after ten years of inflation, you haven't really made a $5 gain in real terms. Lower capital gains rates partially compensate for the inflation tax.

Double taxation: Corporate profits are taxed at the corporate level, then taxed again when distributed as dividends or reflected in higher stock prices. Lower capital gains rates offset this.

These arguments are real. But they apply to actual investment risk like putting capital into something productive and uncertain. They don't apply to inherited wealth sitting in index funds, or private equity using borrowed money to buy companies and fire people, or the carried interest loophole that lets hedge fund managers classify their labor income as capital gains.

Private equity and hedge fund managers typically earn compensation in two ways: a management fee (usually 2% of assets under management) and carried interest (usually 20% of profits).

The management fee is taxed as ordinary income. The carried interest, a share of profits for managing other people's money, is taxed as capital gains, the lower rate. But the fund manager didn't put that capital at risk. They managed someone else's capital. It's labor income dressed up in a capital gains costume.

This has been called one of the most indefensible provisions in the tax code by economists across the political spectrum from left to right. Obama campaigned on closing it. Biden campaigned on closing it. Trump complained about it. It has never been closed. The private equity lobby is very, very good at keeping it alive.

Why Is the Code 70,000 Pages Long?

Because every one of those pages represents a deal someone made.

The tax code is not primarily a revenue-collection document. It's a legislative history of every industry, interest group, and donor class that successfully lobbied Congress to carve out an exception, deduction, credit, or exclusion for their specific situation.

The mortgage interest deduction: a gift to the real estate and banking industries, framed as helping homeowners. The research and development tax credit: originally sensible, now a gaming opportunity for tech and pharmaceutical companies. Accelerated depreciation on equipment: lobbied for by manufacturing. Pass-through income deductions: lobbied for by real estate developers, including, most famously, the family that happened to own the White House.

Every exception has a story. Every story involves money. The complexity isn't the result of incompetence it's the accumulated result of successful lobbying over 100+ years.

The Tax Preparation Industry: Conflict of Interest Built In

Intuit (TurboTax) and H&R Block spend millions of dollars every year lobbying against tax simplification. Not in favor of a particular loophole. Just against the idea of making taxes simpler.

In most developed countries, the government already knows what you owe. They send you a pre-filled form. You check it, sign it, done. The IRS already has your W-2s, 1099s, and most of the information it needs to file your return for you. Other countries, Estonia, Denmark, Japan, do this. It takes 15 minutes.

The US doesn't do this. ProPublica investigated why. Intuit and H&R Block successfully lobbied Congress to prohibit the IRS from offering free tax preparation software that would compete with their products. The IRS Free File program, which was supposed to be a free alternative, was structured to be confusing and difficult to find, steering users toward paid products.

They made the process harder for you so you would pay them to navigate the complexity they helped create. LMAO.

The IRS Accuracy Problem Is Real

In 2003, Money Magazine gave the same hypothetical tax return to 46 professional tax preparers. They got 46 different answers ranging from a refund of $47 to a tax due of $1,504. That's not a rounding error; that's a $1,551 spread on the same return.

More recent studies by the Government Accountability Office have found that IRS telephone assistors give incorrect or incomplete answers to basic questions a significant percentage of the time. The National Taxpayer Advocate, an office inside the IRS itself, annually documents how the complexity of the tax code creates compliance burdens that fall disproportionately on ordinary filers, not on wealthy ones who can hire experts.

Is There a Simpler Way? Yes. Several.

The most prominent alternative is the FairTax, which would eliminate the income tax, payroll taxes, and the IRS entirely, replacing everything with a single national consumption tax — a tax on what you spend rather than what you earn. Under FairTax, you'd pay nothing on money you save or invest, and a ~23% inclusive tax rate on consumption, with a monthly 'prebate' to offset the burden on low-income households.

The FairTax has real supporters and real critics. Proponents argue it would eliminate compliance costs, reward saving and investment, and make the underground economy taxable. Critics argue it would shift the burden to middle and lower-income households who spend a larger percentage of their income, and that the 23% inclusive rate (30% exclusive) understates what the rate would actually need to be.

Other approaches: a flat tax (one rate on all income above a threshold), radical simplification of the existing code by eliminating most deductions and lowering rates, or return-free filing where the government sends you a pre-filled return based on the information it already has.

All of these have been proposed. None have gained traction. Because simplifying the tax code doesn't just mean less paperwork, it means eliminating the provisions that benefit powerful people. And powerful people are very good at preventing that.

So Is It Deliberate?

Nobody sat in a room and said "let's make taxes incomprehensible on purpose." It's more pernicious than that. The complexity emerged over decades through a process that rewards organized, well-funded interests over diffuse public ones.

When an industry spends $10 million lobbying for a tax provision that saves them $500 million a year, that's a rational investment. The 100 million people who overpay their taxes as a result each lose maybe $500 individually not enough to organize around, not enough to hire a lobby. So the interests that benefit from complexity get organized representation, and the public interest in simplicity has no equivalent champion.

The tax code is deliberate in the way all institutional dysfunction is deliberate: not planned from the start, but actively maintained by people who benefit from it. Nobody with real influence wants a simpler system because a simpler system serves the public, not them.

And the filing deadline is still April 15. Good luck.

Stay Frustrated